In this article our Senior Corporate Tax Manager, Paul Woodward, reviews the changes and how using a partnership structure could be a potential solution for buy to let investors who incorporate their letting business.

The new mortgage interest restriction rules impact individuals and partnerships with rental income businesses. They do not apply to companies, property dealing or development companies, commercial lettings or furnished holiday lettings.

The change will be phased in over a three year period, and so its full effect will not be felt until 2020. However, at this point finance costs will no longer be allowed as a deduction from property income. Instead, an adjustment will be made to allow a deduction up to the basic rate level. The maximum deduction will therefore be 20% of finance costs incurred.

The following examples illustrate how the restriction will work for a variety of taxpayers. The comparison is made between 2016/17 (the last year in which full deduction was available) and 2020/21 (the year in which full restriction is made).

Example 1

Mr A is a higher rate taxpayer. He has a buy to let property with a relatively small outstanding loan.

| 2016/17 | 2020/21 | |

|---|---|---|

| Gross rental income | 9,000 | 9,000 |

| Less: repairs and other expenses | (2,000) | (2,000) |

| 7,000 | ||

| Less: mortgage interest | (3,000) | |

| Net rental profit | 4,000 | 7,000 |

| Income tax @ 40% | 1,600 | 2,800 |

| Less: interest relief (3,000 x 20%) | (600) | |

| Net tax liability | 1,600 | 2,200 |

Mr A’s liability has increased by £600 as a result of the restriction.

Example 2

Mr and Mrs B are a couple who run a sizeable property rental business in joint names. They have no other income.

They are currently basic rate taxpayers as a result of the significant mortgage interest that they pay.

| 2016/17 | 2020/21 | |

|---|---|---|

| Gross rental income | 650,000 | 650,000 |

| Less: repairs and other expenses | (250,000) | (250,000) |

| 400,000 | ||

| Less: mortgage interest | (350,000) | |

| Net rental profit | 50,000 | 400,000 |

| Income for each partner | 25,000 | 200,000 |

| Less: personal allowance | (11,000) | |

| Income tax @ 20% | 2,800 | 6,400 |

| @ 40% | 47,200 | |

| @ 45% | 22,500 | |

| Less: interest relief (175,000 @ 20%) | (35,000) | |

| Net tax liability per partner | 2,800 | 41,100 |

Mr and Mrs B have a much increased tax liability because they have lost their entitlement to a large proportion of mortgage interest relief, are now higher rate taxpayers and no longer qualify for tax free personal allowances.

They have no other income and their tax liabilities now exceed their rental profits meaning they will soon be a position where property will have to be sold to pay tax liabilities.

Example 3

Mrs C has earned income of £25,000. She has a rental property on which she receives gross income of £30,000 and has a large mortgage on which she pays interest of £30,000.

| 2016/17 | 2020/21 | |

|---|---|---|

| Earned income | 25,000 | 25,000 |

| Rental income | 30,000 | 30,000 |

| 55,000 | ||

| Less: mortgage interest | (30,000) | |

| Total income | 25,000 | 55,000 |

| Less: personal allowance | (11,000) | (11,000) |

| Taxable income | 14,000 | 44,000 |

| Income tax @ 20% | 2,800 | 6,400 |

| @ 40% | 4,800 | |

| Less: interest relief (30,000 @ 20%) | (6,000) | |

| Net tax liability | 2,800 | 5,200 |

The rental business is breaking even and Mrs C and is a basic rate taxpayer so it could be assumed that the new rules would not impact on her. But due to the operation of the restriction she ends up paying £2,400 income tax on a non-profitable business.

These three examples show that tax liabilities will be much increased in the future for income tax paying rental businesses and the impact of these extra tax bills could mean that properties have to be sold.

The challenge of moving property into a company structure

With the above examples in mind, I think we can clearly see the negative impact that the new rules will have on buy to let investors.

The good news is that these interest restrictions do not apply to corporate structures.

However, before you rush off to your accountant to incorporate your property letting business, there are some stumbling blocks that could halt you in your tracks.

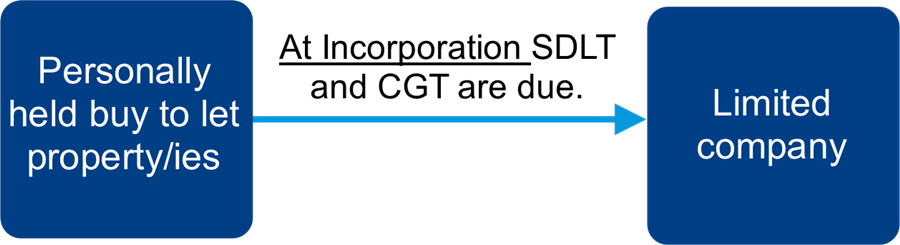

In particular, capital gains tax (CGT) and Stamp Duty Land Tax (SDLT) will become due on incorporation.

Stamp Duty Land Tax (SDLT)

The transfer of a property into a company would normally give rise to a SDLT charge. You will also be liable for a 3% SDLT surcharge meaning your tax bill could wipe out the benefits of incorporation.

For example, if you were to move two rental properties valued at £300,000 each into a limited company you would be liable for £28,000 Stamp Duty on incorporation. The ongoing savings from incorporation would therefore need to be weighed up against this initial tax charge.

Capital gains tax (CGT)

When a property business incorporates, the transfer of properties from the existing business to the new company is a chargeable event for capital gains tax purposes.

The gain would normally be calculated as the difference between the purchase costs and the value of the property at the date of transfer (less any incidental costs or enhancement expenditure that has been incurred). This is therefore a major issue for incorporating businesses as you could end up with a dry CGT bill – tax to pay but no proceeds received.

Fortunately businesses can usually benefit from incorporation relief which in essence defers any gain until the shares in the company are sold.

The challenge with securing incorporation relief is that it requires a business, and the passive letting of property is not classed as a business. The activities undertaken must therefore be over and above those usually offered by a landlord and HMRC will look at the amount of time spent on the rental business. The current thinking is that at least 20 hours per week needs to be spent on business issues. You can check the availability of incorporation relief with HMRC in advance so you can be certain that a CGT charge will not arise before the incorporation is undertaken.

There are also other factors and we usually provide professional advice to clients before they make a decision on incorporation.

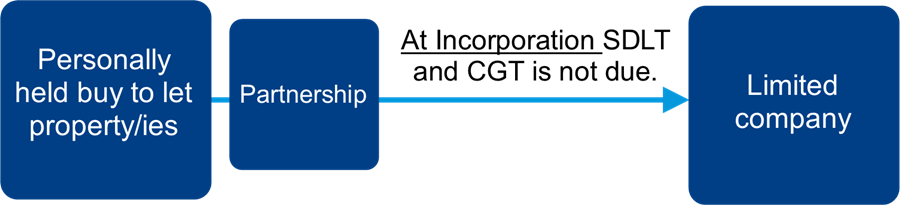

A potential solution: Using a partnership structure to facilitate incorporation

There is a potential solution to transferring your property to a corporate structure that doesn’t leave you exposed to SDLT liabilities; using a partnership structure as an intermediary.

If we look at the incorporation of a bona fide partnership there are special rules that remove the charge to SDLT as long as the ownership proportions in the partnership and the new company are the same.

The partnership must be a bona fide partnership i.e. there must be a partnership agreement in place, a partnership bank account and genuine profit sharing. There are also anti-avoidance provisions in place that catch partnerships being formed solely for incorporation purposes meaning the partnership must be in place for a certain period of time.

Paul comments, “The property must be left in the partnership for a period time, during which the business will see a reduction in the mortgage interest relief it receives. It is therefore important to decide if this structure is right for you and allow time to incorporate the partnership before the full reduced relief comes into full affect from 2020.”

Paul comments, “The property must be left in the partnership for a period time, during which the business will see a reduction in the mortgage interest relief it receives. It is therefore important to decide if this structure is right for you and allow time to incorporate the partnership before the full reduced relief comes into full affect from 2020.”

Further buy to let articles

Please note that we are currently unable to assist new clients with regards to buy to let/rental property tax services or advice. You can find further articles and factsheets here from our team, that may be of interest.

With more than 20 years in tax, Paul provides tax compliance and advisory services to clients, and specialises in R&D and capital allowance claims.