1. Understanding Your UK Tax Residency Status

Before leaving the UK, you’ll need to determine whether you will remain a tax resident after your move. The UK uses the Statutory Residence Test (SRT) to establish residency, based on factors such as time spent in the UK and your ties to the country:

Some of the key elements include:

- 183-day rule: If you spend 183 days or more in the UK during a tax year, you are considered a UK tax resident.

- Fewer than 16 days: If you spend fewer than 16 days in the UK, you may qualify as a non-resident.

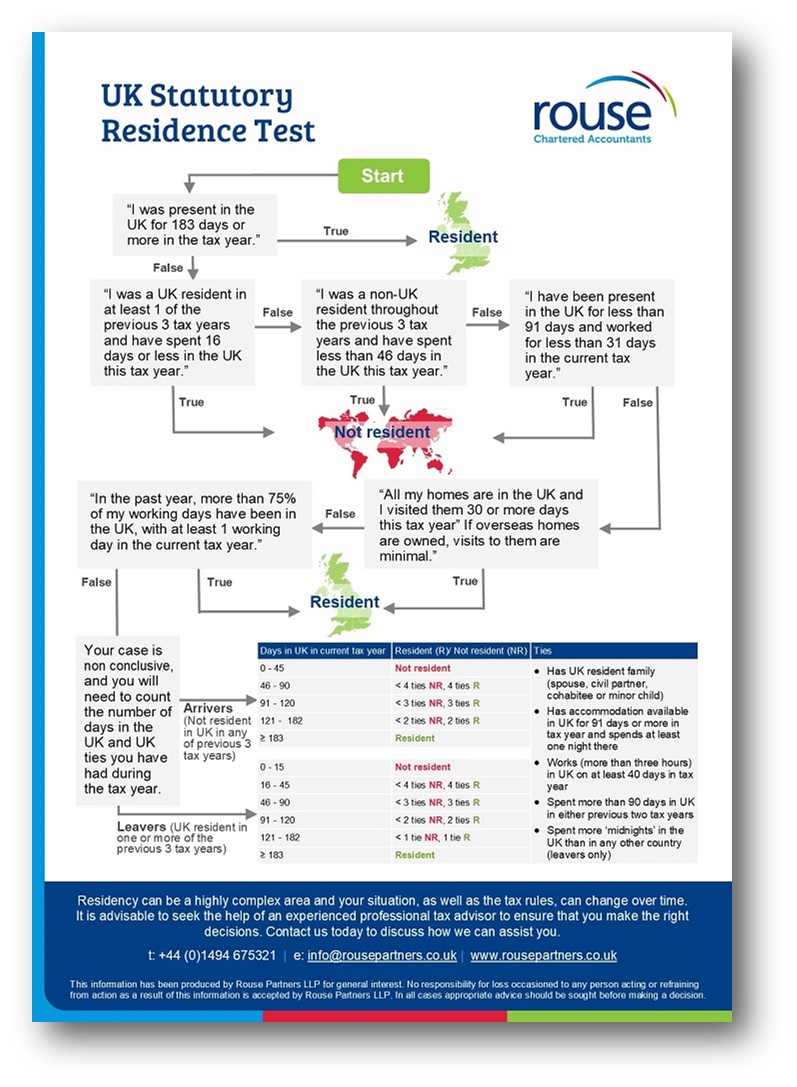

In between: Where none of the automatic tests are satisfied, the situation becomes more complicated and requires your ‘ties’ to the UK to be identified. We have prepared a handy flowchart to take you through the considerations which you can find here – Statutory Residence Test (SRT).

In between: Where none of the automatic tests are satisfied, the situation becomes more complicated and requires your ‘ties’ to the UK to be identified. We have prepared a handy flowchart to take you through the considerations which you can find here – Statutory Residence Test (SRT).

If you leave partway through the year, Split Year Treatment may apply, allowing you to be treated as a UK resident for part of the year and non-resident for the remainder.

Determining your tax residency can be a highly complex area and your situation, as well as the tax rules, can change over time. Contact our experienced team of tax advisors for assistance.

2. Income and Capital Gains Tax: How leaving affects you

One of the most significant changes when leaving the UK is how your income and assets will be taxed.

- Income Tax: Once you become a non-resident, you will generally no longer pay UK tax on overseas income. However, UK-source income, such as rental income from UK property or earnings from UK businesses, will usually remain taxable in the UK.

- Capital Gains Tax (CGT): As a non-resident, you typically do not pay UK CGT on disposal of non-UK assets. However, disposals of UK property may still be subject to Non-Residents Capital Gains Tax (NRCGT), so if you own UK real estate, plan accordingly.

3. Pension and benefit implications

- UK Pensions: If you receive a UK state pension or private pensions, these will generally still be taxed in the UK, though the tax treatment may vary based on tax treaties between the UK and your new country of residence. You may be eligible for a tax credit or exemption under a Double Taxation Agreement (DTA).

- National Insurance (NI): If you cease working in the UK, you will no longer be required to pay UK National Insurance contributions. However, keeping up with voluntary contributions might be important if you plan to return to the UK in the future or wish to protect entitlement to certain benefits or the state pension.

4. Double Taxation Agreements (DTAs): Avoid paying double tax

The UK has signed Double Taxation Agreements with many countries to prevent double taxation – meaning you won’t pay tax on the same income in both the UK and your new country of residence. The exact terms of these agreements can vary, so it’s important to review the specific treaty between the UK and your new country to understand how your income (such as salary, investments, and pensions) will be taxed.

5. Inheritance tax: What happens to your estate?

The UK has moved away from a domicile-based approach to Inheritance Tax (IHT) and instead applies a residence based system. Under the new rules, IHT generally applies to an individual’s worldwide assets while they are UK resident, rather than based on domicile alone.

Once you become non UK resident, your exposure to UK inheritance tax on non UK assets may reduce over time. However, UK based assets such as UK property will typically remain within the scope of UK IHT regardless of your residency status.

It’s also important to be aware that “tail” provisions may apply, meaning IHT exposure can continue for a period after you leave the UK, depending on your length of prior UK residence. As a result, leaving the UK does not necessarily remove IHT liability immediately.

Given the complexity of the new residence-based rules, careful planning is essential to understand when and how UK IHT exposure may fall away, particularly for individuals with significant international assets.

6. Exit Tax: Deemed disposals and capital gains

While the UK doesn’t impose a blanket exit tax, if you are still considered a UK tax resident when you leave, there may be rules regarding deemed disposals. This means that you might be treated as having sold certain assets (like shares) when you leave the UK, triggering Capital Gains Tax on any increase in their value up until that point.

7. Reporting requirements: Keep HMRC in the loop

When you leave the UK, it is important to notify HMRC. This is typically done by completing a P85 form, which informs HMRC of your departure and helps determine your tax position for the year.

Additionally, if you are still earning income from UK sources (e.g., rental income), you may need to file a UK tax return to declare this income and ensure you are paying the correct amount of tax.

8. Banking, investments and foreign income

- UK bank accounts: If you continue to maintain a UK bank account after leaving, be aware that interest or investment income from UK based sources may still be taxable in the UK. You should also notify your bank about your change in residency.

- Foreign income: As a non-resident, your income from outside the UK will generally not be subject to UK tax. However, you will need to ensure you are meeting the tax obligations in your new country of residence.

Your checklist for leaving the UK

When planning your move, here’s a summary of the steps you should take to ensure a smooth transition from a UK tax resident to a non-resident:

| Action point | Status |

| 1. Determine your tax residency status based on the Statutory Residence Test. | |

| 2. Complete the P85 form to notify HMRC of your departure. | |

| 3. Review your income, investments, and capital gains position to understand how these will be taxed. | |

| 4. Consider your pension and National Insurance contributions, and make any necessary arrangements. | |

| 5. Understand Double Taxation Agreements between the UK and your new country to avoid double taxation. | |

| 6. Review your inheritance tax obligations, particularly if you own UK based assets. | |

| 7. Stay on top of your reporting requirements with HMRC, especially if you still have UK income. |

Need help navigating your tax status?

Leaving the UK and moving abroad can bring about significant tax considerations. Our personal tax team has significant experience advising clients on tax residency, and we can support and guide you through the process.

Contact us today to schedule an initial consultation to find out how we can support you.

Leo advises on personal tax compliance and planning, with expertise in tax residency, cross-border issues, capital gains tax and director responsibilities.