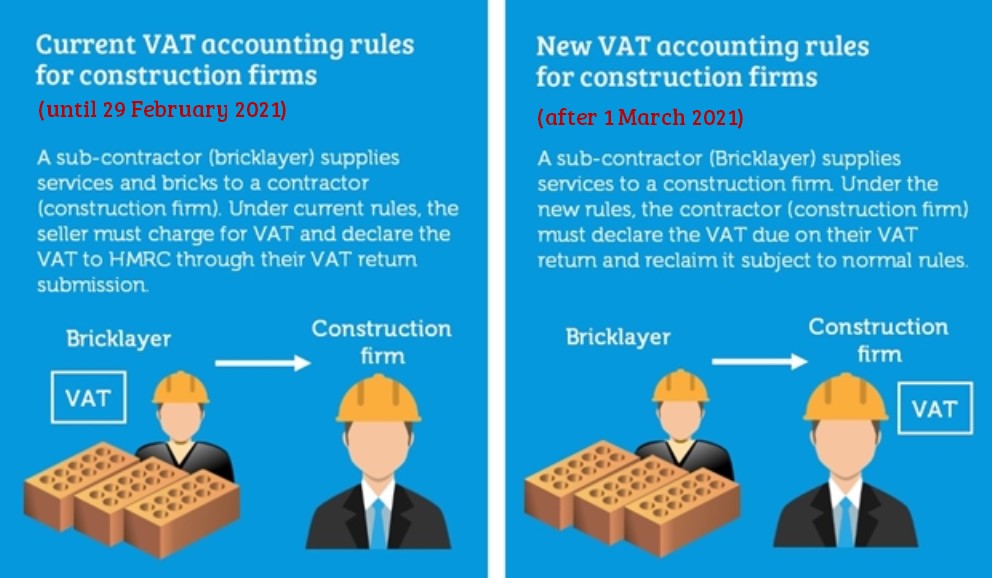

What is changing?

From 1 March 2021, new ‘reverse charge VAT accounting’ rules apply to all qualifying supplies made on or after that date. This means that:

- Suppliers of goods or services are no longer be involved in the payment of VAT to HMRC. The liability for VAT payment is now be with the VAT registered customer.

- The customer must declare the VAT due as output tax on their own VAT return and reclaim it subject to normal rules via the reverse charge mechanism (though supplies to the final customer are excluded, see further exclusions below).

An example

Why was this change made?

HMRC is aiming to reduce ‘missing trader fraud’ where a supplier charges and collects VAT, but then do not pay it to HMRC. It believes that this is an area where it incurs substantial tax loss.

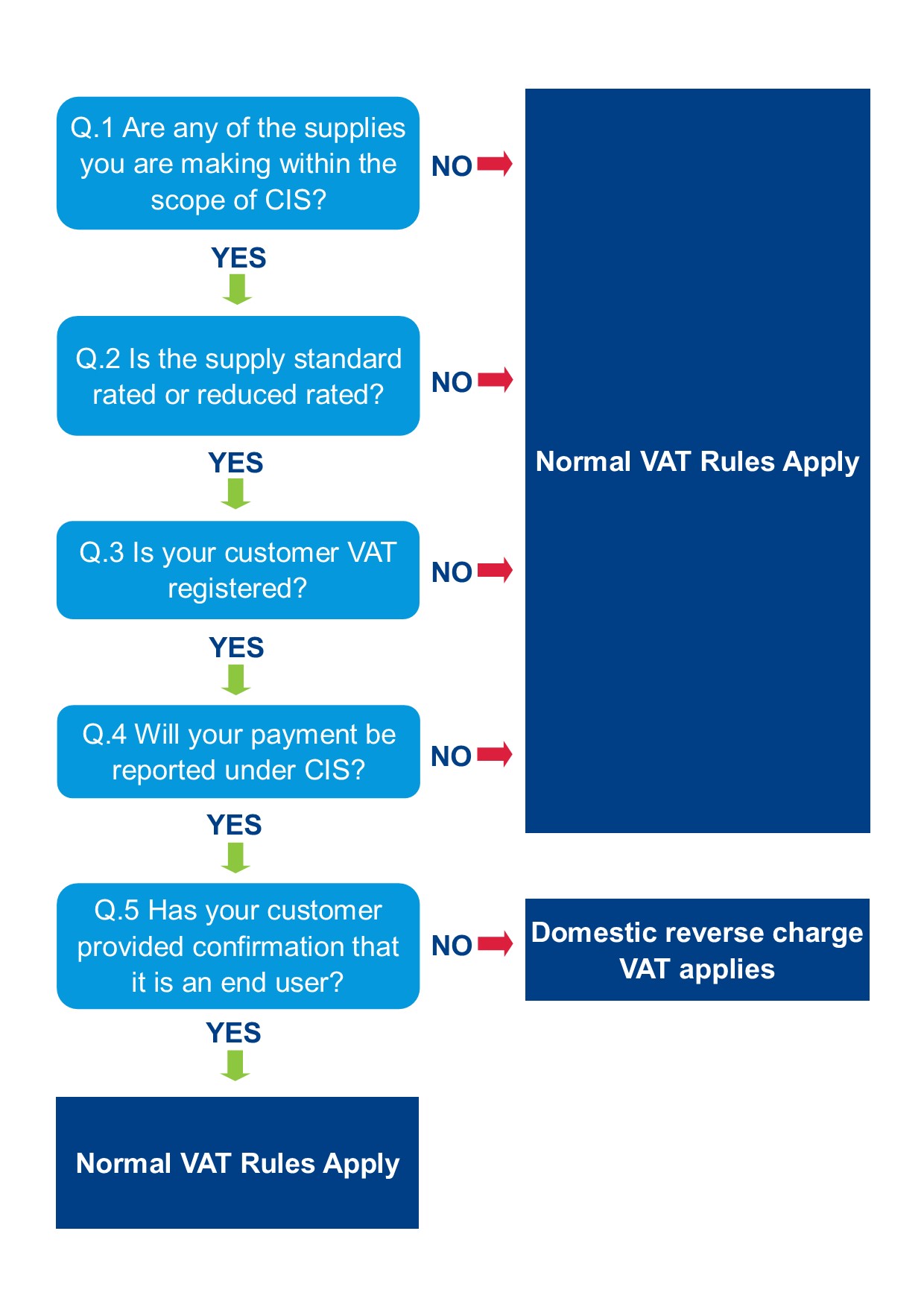

Deciding what is and isn’t applicable

We have a flowchart below (developed by HMRC) which you can use to assist your decision making on whether to apply the VAT reverse charge:

Who will be impacted?

The change is far reaching and impacts directly on all contractors and sub-contractors who supply construction services (as covered by the Construction Industry Scheme).

It is estimated that this will lead to major administrative changes for some 100,000 to 150,000 businesses in the sector, including many small construction firms.

This will include:

- General construction: Construction, alteration, repair, extension, demolition or dismantling of buildings or structures (whether permanent or not);

- Groundwork construction: Construction, alteration, repair, extension or demolition of any works forming, or to form, part of the land, including walls, roadworks, power-lines, electronic communications apparatus, aircraft runways, docks and harbours, railways, inland waterways, pipe-lines, reservoirs, water-mains, wells, sewers, industrial plant and installations for purposes of land drainage, coast protection or defence;

- Renovations and maintenance: painting or decorating the internal or external surfaces of any building or structure, site clearance, earth-moving, excavation, tunnelling and boring, laying of foundations, erection of scaffolding, site restoration, landscaping and the provision of roadways and other access works;

- HVAC: Installation in any building or structure of systems of heating, lighting, air-conditioning, ventilation, power supply, drainage, sanitation, water supply or fire protection;

- Cleaning: Internal cleaning of buildings and structures, so far as carried out in the course of their construction, alteration, repair, extension or restoration.

But this will not include:

- Direct to consumer sales: It will exclude supplies to the final customer or those not in the construction sector, such as a high street retailer;

- New home construction: The construction of new homes (flats or houses) will not be affected as this is “zero rated” and therefore no VAT is liable;

- Internal supplies: Any connected parties (should as a corporate group) or supplies between landlords and tenants;

- Building supplies: Manufacturing of building or engineering components or equipment, materials, plant or machinery, or delivery of any of these things to site. Also, manufacturing of components for systems of heating, lighting, air-conditioning, ventilation, power supply, drainage, sanitation, water supply or fire protection, or delivery of any of these things to site;

- Architectural services: The professional work of architects or surveyors, or of consultants in building, engineering, interior or exterior decoration or in the laying-out of landscape;

- Signage: signwriting and erecting, installing and repairing signboards and advertisements;

- Security: The installation of security systems, including burglar alarms, closed circuit television and public address systems;

- Certain fixtures: The installation of seating, blinds and shutters.

What is the impact?

Nicola comments, “The greatest impact is likely to be on cashflow. When applying the reverse charge, construction businesses will have to wait to recover the VAT via their VAT returns. This creates a delay that will hit working capital, which is so often the lifeblood of construction businesses.”

“Then there is the increased admin burden and decisions that need to be made by both suppliers and customers. When acting as the supplier of construction services, for each job you will need to consider the type of work, if the sale is to an end user or third party, and whether they are VAT registered. This will create a lot more admin time for suppliers.”

“For the customer purchasing construction services, they need to check that they have been charged VAT correctly, or account for the VAT due accordingly. Incorrectly charged VAT is not recoverable and penalties may also be issued for incorrectly accepting VAT invoices. In my experience contractors tend to act cautiously to do the right thing, but it is important that they review and query any purchases that shouldn’t incur the reverse charge, such as zero-rated work e.g new build projects.”

“There are a whole host of considerations that now must be made, from how to deal with customers that apply CIS, whether terms and conditions, PO’s and work orders need to be amended or reviewed by a professional, and how to assess the correct VAT treatment of purchases. You also need to decide how you will keep evidence to support the day-to-day decision you are making to minimise the risk of HMRC penalties.”

“Ultimately, it is important that customers communicate with suppliers during the tendering and contracting process to ensure the correct VAT treatment.”

“The VAT reverse charge isn’t something that can just be passed to your accountant or tax advisor to deal with. It spans both accounting and your own internal processes, so you need to work together to plan the changes and then communicate with your team”, comments Nicola.

Contact our construction accountants

Contact our team of construction accountants who can assist you with these VAT changes, as well as the wider range of support that we can offer your construction business.

With a career in VAT spanning over 20 years, Nicola advises businesses of all sizes; from start-ups to major international organisations.